According to the new Nordic defence tech report from Dealroom and Danske Bank, the region’s defence and dual-use startup ecosystem is now worth about 5.4 billion dollars, almost five times more than in 2019. VC investors have put in roughly 1.7 billion USD since 2019 across more than 150 companies.

The report notes that “the EU and Nordic countries are sharpening their defence and dual-use technology strategies, aligning industrial policy, innovation funding, and security goals.”

On the surface, that looks like a success story. Nordic governments are raising defence budgets, talking about stockpiles, resilience, and NATO readiness. The startup side seems to be waking up in parallel.

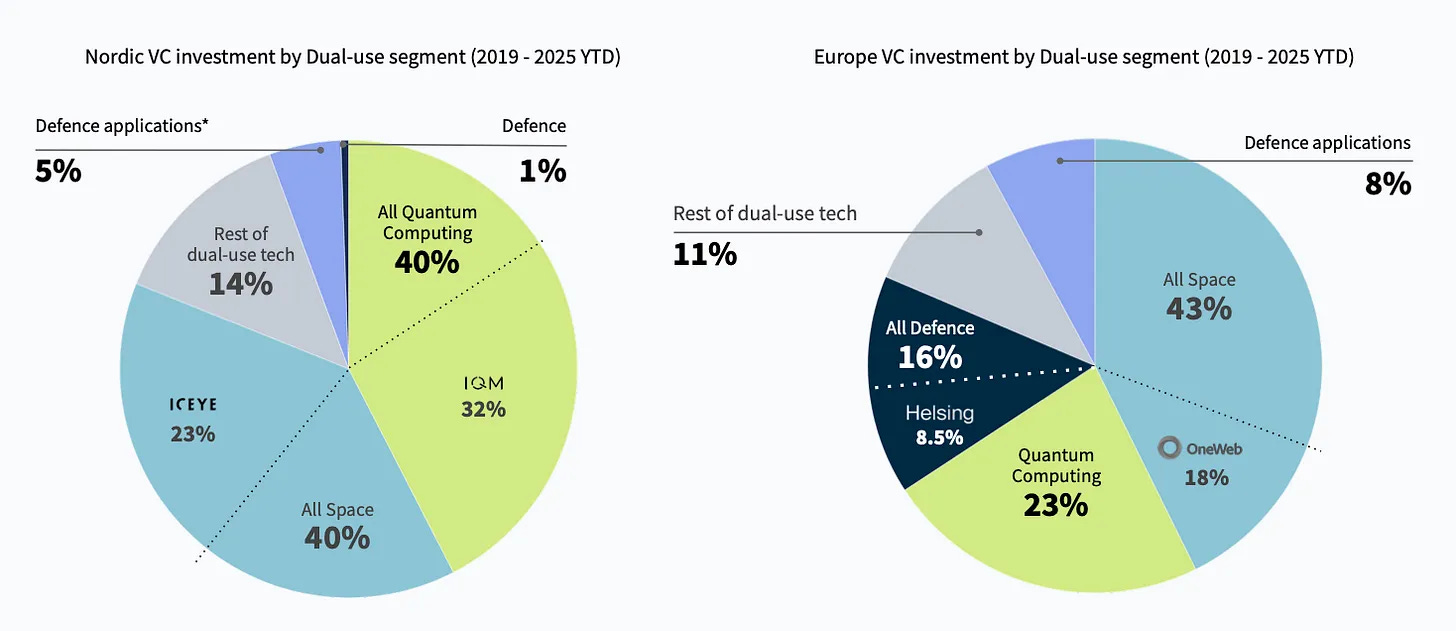

Look a little closer and a different story appears. Most of that private money is not going into what generals are actually asking for. Around 80 percent of VC funding since 2019 has gone into space and quantum, with only a thin slice going into core defence systems. The charts show the Nordics spending about 40 percent of dual-use VC on space and another 40 percent on quantum, while pure defence gets around 6 percent when you count defence and defence applications. Europe as a whole spends a much larger share on core defence technology such as weapons, sensors, and command systems.

In other words, the Nordics are building satellites and quantum stacks while buying artillery shells and air defence from abroad. That is a strategic choice, but it is also a risk. Space and quantum are long-horizon bets. Ammunition, drones, and ground systems are what Ukraine burns through every day.

Per capita, the region looks strong. The Nordics now lead Europe on defence and dual-use VC per head, with Finland way out in front. Finland and Denmark also sit at the top of the European tables for quantum investment, and Finland has turned itself into a serious space player, with major rounds for firms such as ICEYE and IQM. The geographic spread is also telling. Helsinki, Stockholm, Copenhagen, Aalborg, Trondheim, and Oslo form the main cluster, with Aalborg and Odense in Denmark showing the pull of local universities and legacy defence industry.

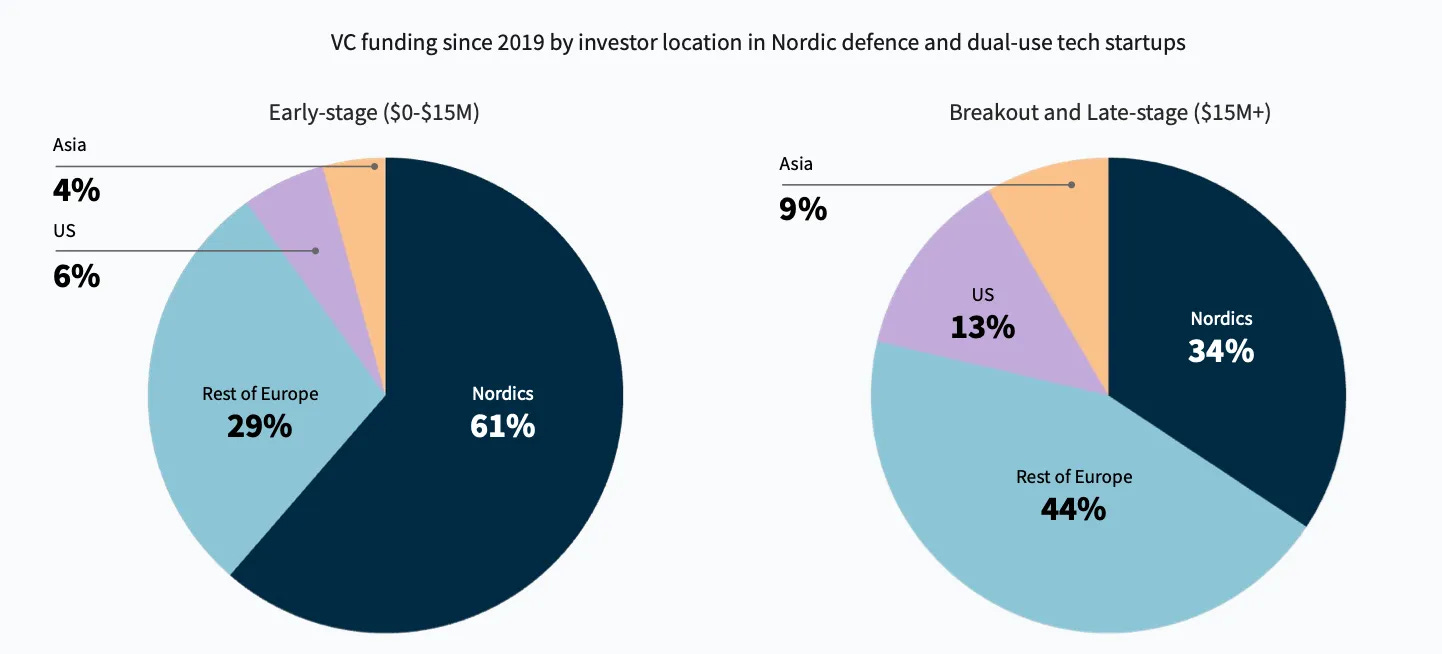

On the investor side, the report shows a clear shift. Nordic funds supply more than 60 percent of early-stage capital in the sector. Once rounds get larger than 15 million dollars, that share drops to about a third, and European and US funds move in. New specialist funds such as Final Frontier, T|Y|R, Varangians, and others are trying to change that, but they are young and still raising their own capital.

The trend lines are positive. Yet the structure of the market is still out of sync with the security debate in European capitals. If the Nordics want to be taken seriously as defence producers, not just as high-minded suppliers of quantum chips and satellite data, a larger share of private money will have to flow into hard military capability. That means munitions, counter-drone, air defence, and training systems that match NATO’s actual war plans, not only its strategy papers. That said, this report points to a surprisingly good start for a set of countries that are now waking up to real threats on their eastern borders.